Some surprising statistics about customer loyalty and my Offer You Can’t Refuse model

So I decided to write this piece, investigating how loyalty, trust, and some other key insights from SRM’s report are key elements of building an ‘Offer You Can’t Refuse (OYCR)’. But before I do that, I wanted to share some general findings first.

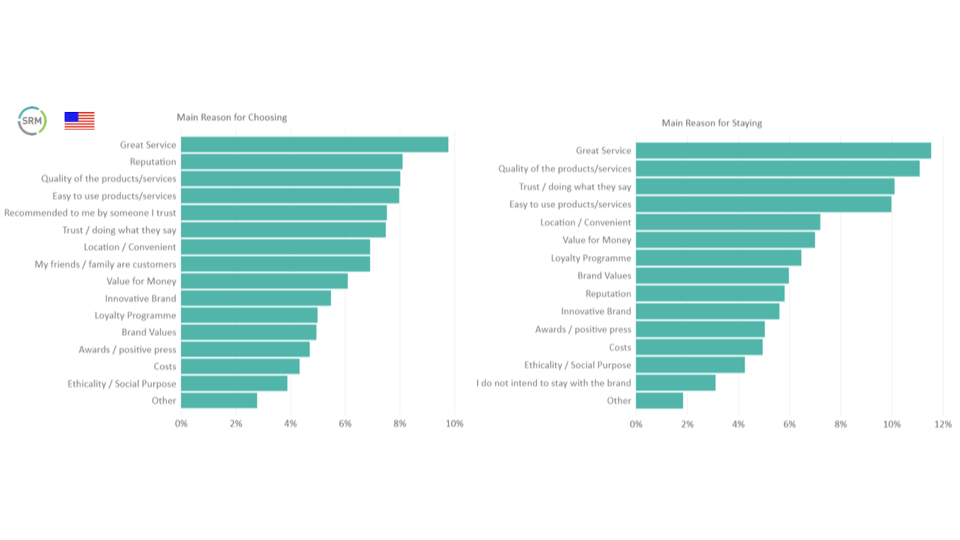

The main reasons for choosing a brand and those for staying and being loyal were not the same within the US and the UK. In the UK, the top 3 reasons to choose a brand are the value for money it gives, the quality of the products or service and their ease of use. So a combination of level one of the OYCR (good product or service) and level two (ease of use). The main three reasons for staying loyal in the UK vary to why customers originally chose the brand: easy to use product is the top one, followed by quality of the products or service and great service.

By contrast in the US, people tend to choose a brand because of great service, easy to use products or services and the quality of the product. So US citizens deem the experience more important for choosing the brand while UK citizens think the price is the most important. In the US, the top three reasons for staying are the same as the ones for choosing, but in a different order (see graphics below).

Good product or service

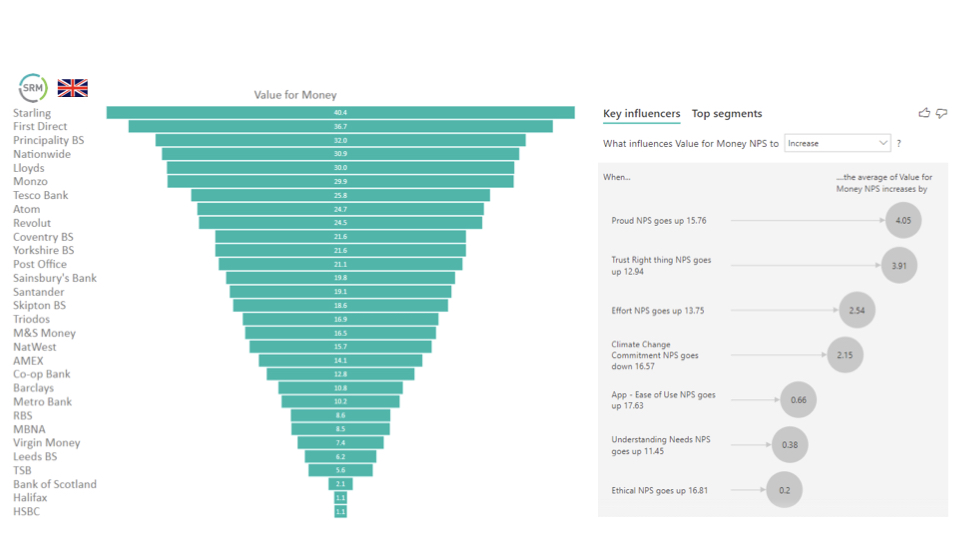

Offering quality products or services is the bare minimum of a successful business, of course. People won’t buy what you offer if it’s bad, right? But that’s not the only thing obviously: Your offering should be reasonably priced, delivering a balanced value for money. Interestingly the “value for money” NPS was deeply connected with some others scores. In the UK the feeling of value for money went up when:

- Consumers trust a brand will do the right things

- They are proud to be associated with the brand

- They think it’s easy to do to business with the brand, with low effort

I’ll let the numbers speak for themselves, but what really struck me is that, in the UK, a higher ‘value for money’ NPS coincides with a lower climate change commitment, showing that those who attach a lot of importance to value for money, are not willing to pay more for products that are better for the environment. Although we still see some (but minor) connection between the increase of the value for money NPS and the increase of the ethical NPS and purpose of the brand NPS.

US citizens have a slightly different take on “value for money.” For them, NPS increases with:

- An easier to use website – so more convenience (stage two of OYCR)

- They trust the brand will do the right thing (linked to stage four of OYCR)

- When consumers think it’s easy to do to business with the brand, with low effort (stage 2 of OYCR)

Digital/transaction convenience

Step 2 of the Offer You Can’t Refuse is the new commodity: If you are unable to offer a fantastic experience through digital convenience, consumers will find other brands that will give it to them.

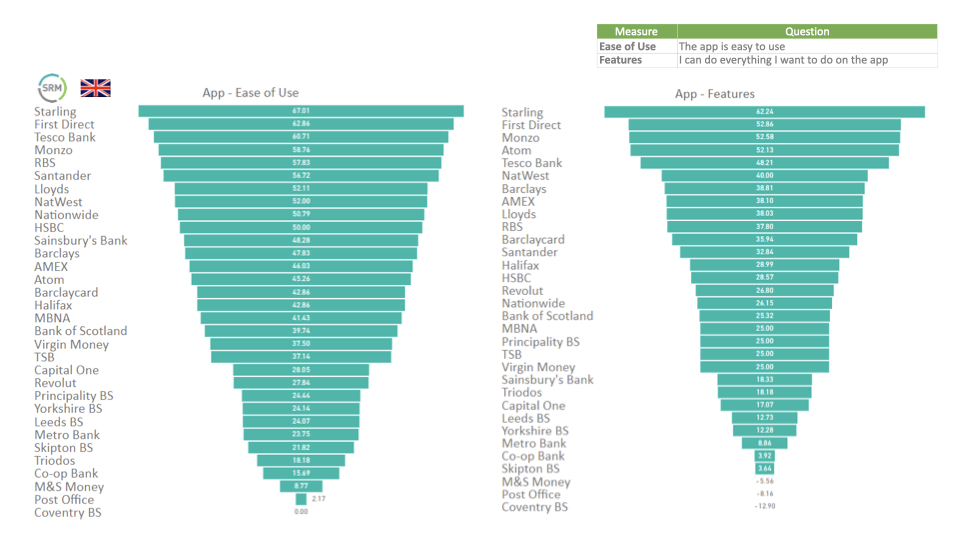

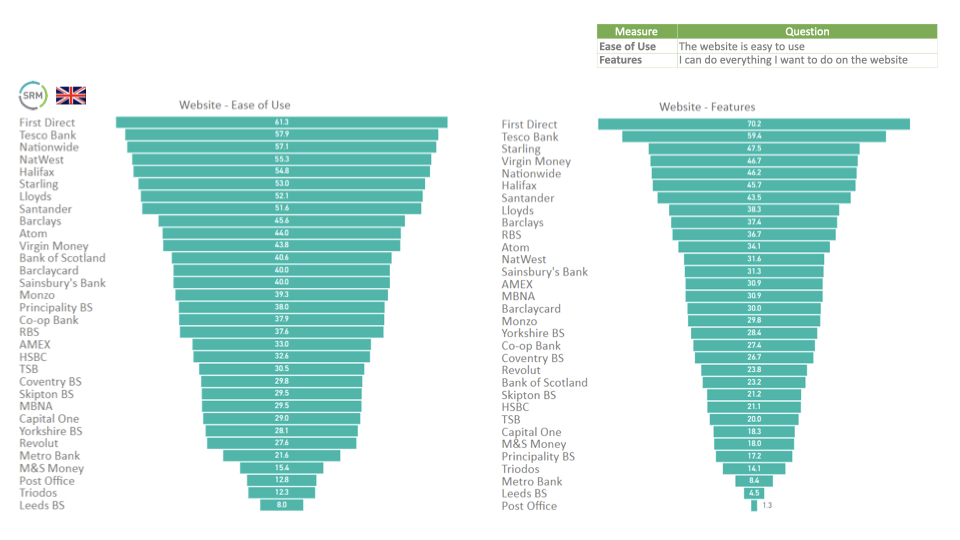

When it comes to the use of apps, UK consumers favor Starling, First Direct and, perhaps surprisingly, Tesco Bank (for ease of use) and Starling, First Direct and Monzo (for breadth of features). Not surprising perhaps is that the top favorites here are neobanks like Starling and Monzo and (internet) retailers like Amazon andTesco. Traditional banks are far further from the top, though there are some exceptions, including First Direct (the telephone and internet-based retail bank division of HSBC Bank), Royal Bank of Scotland, and Santander.

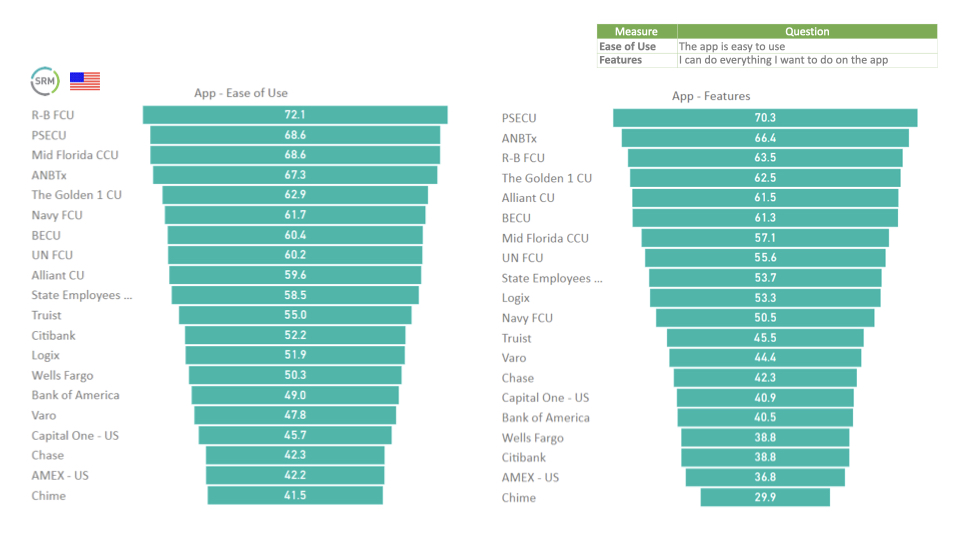

In the US, the mix seems more diverse, when it comes to the features and use of use of the apps:

These, then, are the favorite websites for ease of use and breadth of features, as assessed by UK customers:

And these are the favourites for US customers:

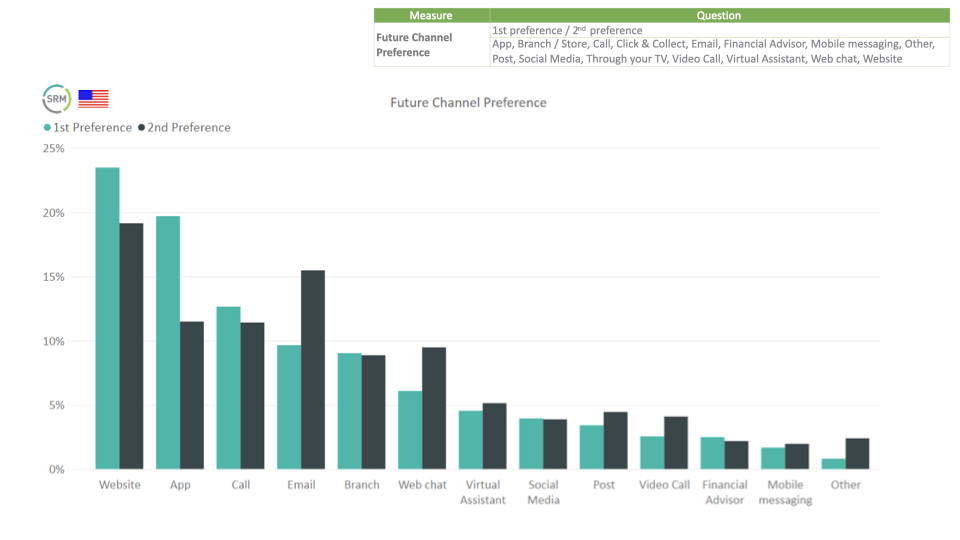

When it comes to channel preferences in both regions, it is safe to say that my “when digital becomes human” still stands, requiring a good mix of both types of channel as you can see below. Unsurprisingly, both in the US and the UK, people seem to prefer websites, app and only then human calls. But in the UK, a branch visit tops at number four, while US citizens prefer email (followed by a branch visit).

In the UK and the US, it’s very clear that the trust in, and loyalty for, brands increases when the effort customers feel they have to make to engage with the brand – the friction – goes down. The easier it is to use the website or the apps, the more this loyalty goes up. This should not really come as a surprise, but now we have the numbers to back that up.

Emotional convenience or Partner in Life

Part three of the Offer You Can’t Refuse is about going far beyond just offering great products, services and experience: it’s about offering emotional convenience, about becoming a Partner in Life for your customers by helping to answer their hopes and dreams.

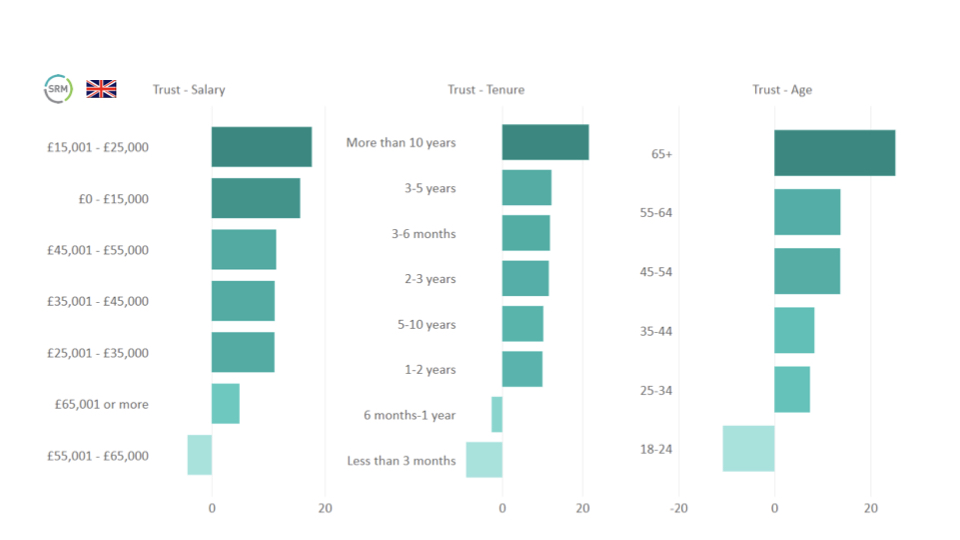

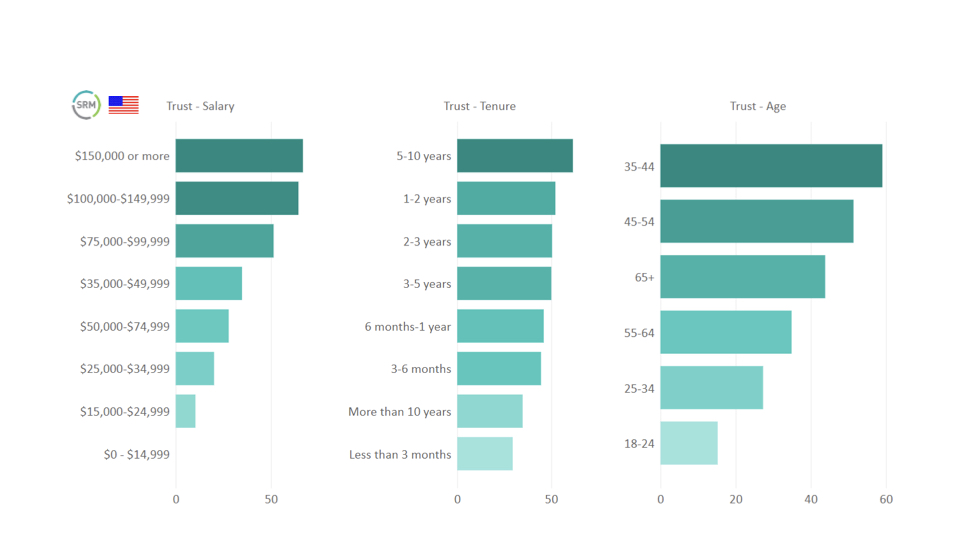

It says a lot that loyalty always increases when customers feel that brands really care about their individual customer needs – in the UK (NPS goes up by 3.44) and also in the US, although to a lesser extent (NPS goes up by 1.39) – and when they trust that brands will do the right thing and act in their favour. This does vary, however, by salary, age, and the tenure of being a customer, as detailed below:

Saving the world

The last step of my Offer You Can’t Refuse model is the one where consumers are increasingly expecting brands to solve world problems that will have a significant impact on their future lives and that of their children and grandchildren, including climate change and global health hazards (the current pandemic, floods, climate migration, droughts and fires etc.)

It should not come as a surprise that trust in brands increases, together with the rise of their ethical NPS and their purpose, both in the UK and the US, the latter being slightly more extreme. What really struck me here, though, was that in the UK the loyalty NPS increased when brands had a lower purpose and a lower commitment to climate change. Especially when you realize that brands do receive higher loyalty in the US when their climate change commitment goes up. It seems that the awareness around the saving the world part, purpose, and climate change is higher in the US than in the UK or perhaps an inherent cynicism within UK customers whether brands are actually delivering against their commitments.

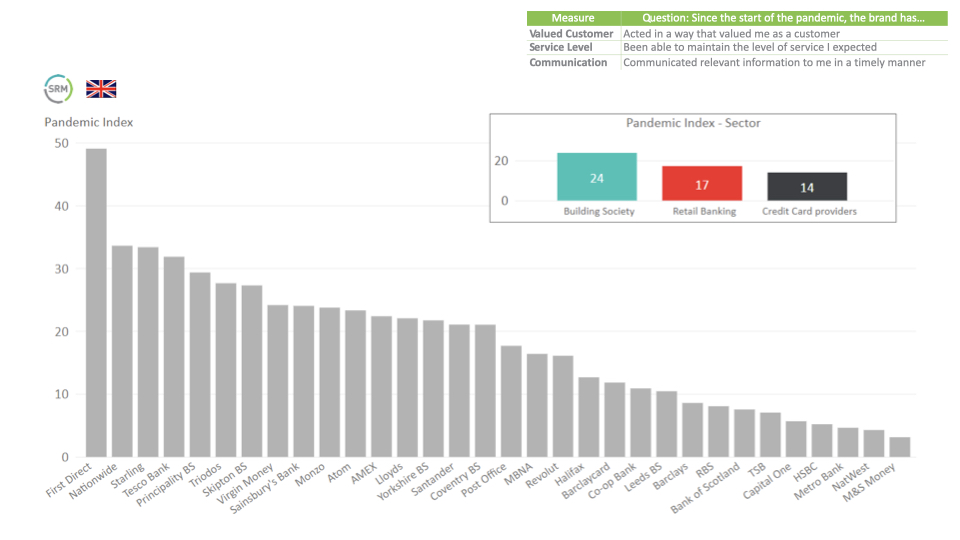

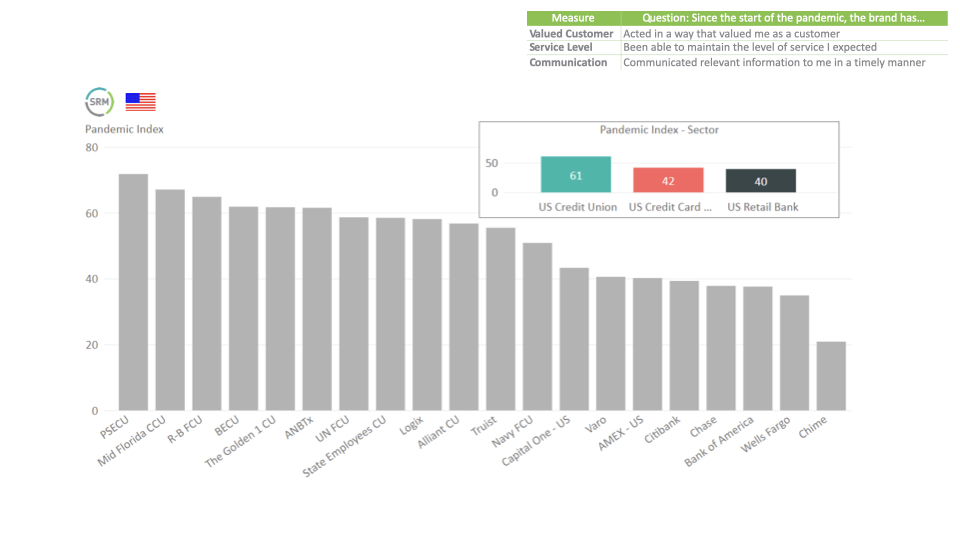

In the US, customers also seemed more satisfied with how brands valued them, maintained their level of service, and communicated to them critically during the pandemic, than in the UK (as you can see):

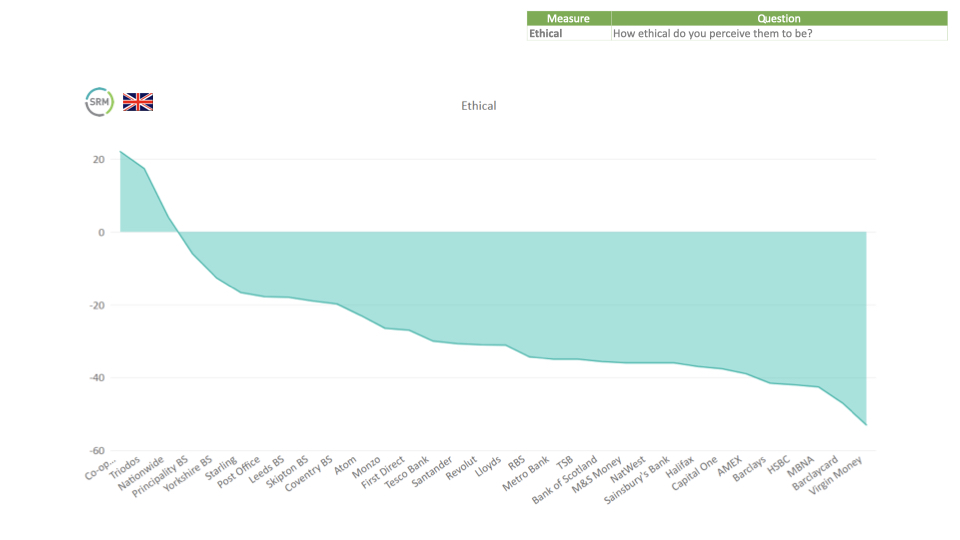

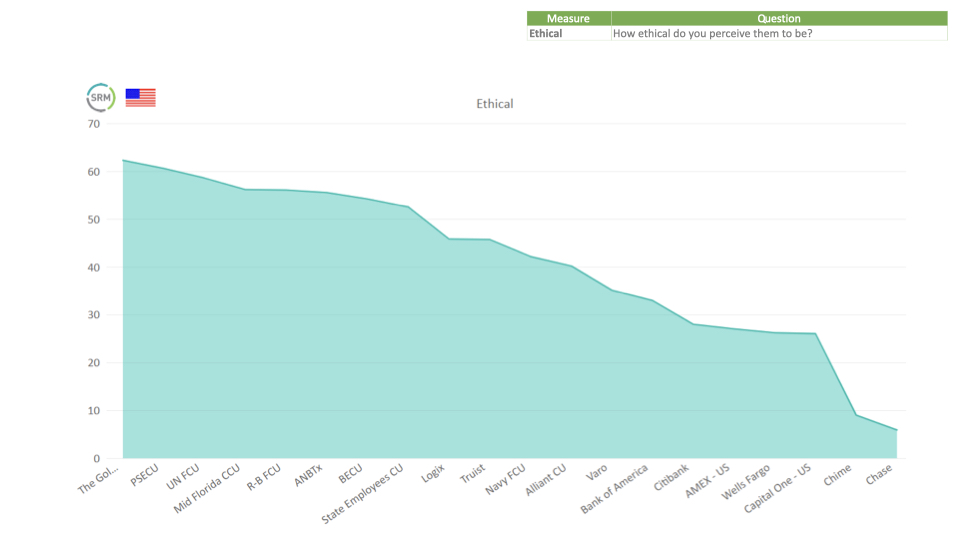

We see that same differences occur (maybe with an even bigger impact) when it comes to perceiving how ethical brands are: the numbers in the UK are much lower and even turn negative, while trust in a brand’s ethics seems a lot higher in the US. The cultural differences between the countries are possibly the driver of these differences:

The same gap between the UK and the US goes for customer purpose and brand purpose. In the UK only Triodos customers overall seek out brands that demonstrate a commitment to positive social impact and also feel that Triodos is actually making an impact. Customers of Co-op Bank believe, too, that it has a strong brand purpose (though their customers don’t prioritise it to the same extent).

US customers demonstrate a higher commitment to a brand’s purpose, as well as a belief in the social impact of brands.

So overall, the most important conclusions of SRM’s research for me are these:

- Customer loyalty is indeed driven by the four pillars of my Offer You Can’t Refuse model

- All the different types of KPIs – trust, loyalty, price/quality ratio, ease of use… – are heavily interlinked and very often, when one of them goes up, so do the others

- Some aspects, especially trust in brands and the importance attached to social impact and purpose, are highly regional still: in this case the US numbers were a lot higher than the UK ones, and I expect this imbalance to be seen between other regions as well

So, thanks a lot to SRM for the crystal-clear insights. if you would like to know more, or book a time to discuss the findings, please contact Jehan Sherjan (jehansherjan@srmeurope.com).